The Unprecedented Nature of Scaling Finance in the Pacific

Tags

The Pacific region a decade ago had low levels of financial inclusion and no mobile money or agent banking services. The UNCDF Pacific Financial Inclusion Programme (PFIP) team saw great potential in both mobile money and agent banking models to lower the cost of distributing financial services to the communities spread across the vast island chains of the South Pacific. However, the programme had fundamental questions about if costs could be lowered enough to reach the outer islands and rural villages, and if any of these countries had large enough populations to support business models, which generally rely on high volumes of transactions to generate profits and thus sustainability.

Over the past decade UNCDF through PFIP has partnered with every major telecom and bank brand in the South Pacific to explore the potential of these models. In Fiji, with the support of PFIP, Vodafone launched M-PAISA and Digicel launched Digicel Mobile Money in 2010. These were the first mobile money services in the Pacific, and they showed exciting potential given 25% of the population had registered for mobile money by December of that year [1]. Further, PFIP worked with BSP Rural, Westpac Instore Banking, and ANZ goMoney to extend agent banking services. Each of these services also showed significant promise registering over 100,000 customers [2] .

However, with the notable exception of M-PAiSA in Fiji, all these services have had trouble standing the test of time. Each one has downscaled significantly or discontinued operations after these initial periods of success. These experiences lead us back to the initial questions on the viability of these models in small island nations. However, we now have the benefit of a decade of data to benchmark the region against the global experience, which we do systematically in the report titled, Viability of Mass Market Digital Financial Services in the Pacific.

The research clearly shows that demand for financial services in Fiji, Vanuatu, Samoa, Tonga and Solomon Islands (data not available for PNG) is in line with other countries of similar income-levels. However, in many cases it is still predominantly served informally. The supply side analysis yielded more complex results indicating that unprecedented efforts are needed to support the private sector to manage these operations sustainability.

Mobile Money in Small Countries

Findex 2017 is the most recent global survey on financial inclusion. It shows that it has been difficult to scale mobile money globally. Of the 90 countries with mobile money services in 2017, only 27% of them had at least 20% of adults using a service, meaning it is difficult to make this model work in most places. However, it was surprising and encouraging to learn that there are a significant number of small countries that have scaled mobile money effectively. Of the 25 known countries where at least 20% of adults are registered for mobile money, seven [3] (28%) have populations under five million people, including Eswatini with a population of just 1.1 million.

Therefore, while scaling mobile money in small countries is more prevalent than commonly understood, there are no known countries as small as Fiji, Vanuatu, Solomon Islands, Samoa or Tonga where services have sustainably scaled to at least 20% of the population. Sustainable mobile money services in any of these countries would be unprecedented. The two following analyses describe the order of magnitude of this challenge.

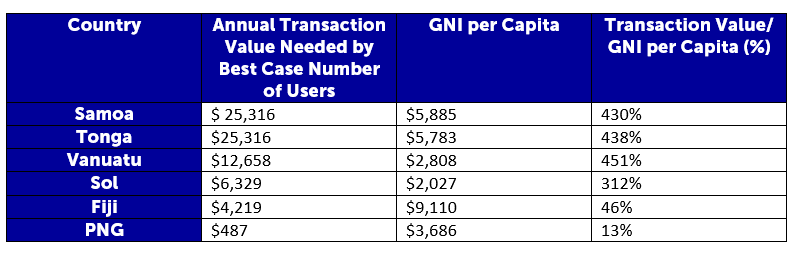

Unachievable Transaction Values

A common benchmark used in the mobile money industry for determining the break-even point of a service is when the service is conducting between US$2 billion to US$3 billion in annual transaction value [4]. Assuming a best-case scenario of 79% of adults adopting the service in each country (as in Eswatini) [5] , means that this would require more than 300% of GNI per capita in four of the six PICs to be transacted through the system annually. Therefore, using this transaction value benchmark, it would be extremely unlikely for a provider to break even in these four countries.

Transaction values needed by adult in each PIC

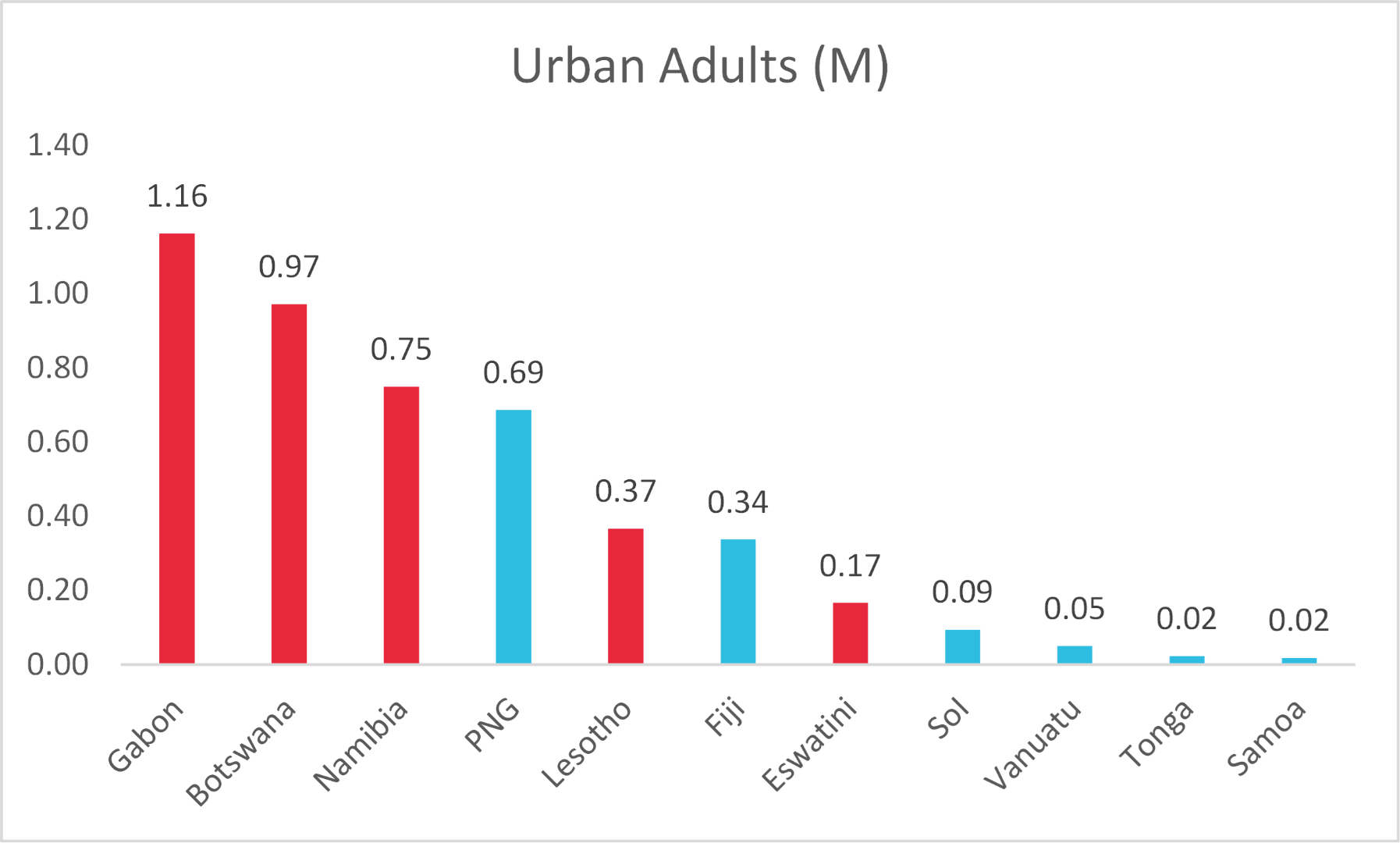

The Limits of Rural Reach

When assessing the business model for mobile money it is also important to analyze the total addressable market (TAM) of urban adults. This is because there has been very limited success operating mobile money or agent banking in rural areas. Kenya has leading mobile money and agent banking models, yet a geospatial analysis of agents by Cenfri showed that in 2015, 84% of mobile money agents and 81% of bank agents were within five kilometers of an existing depositing-taking locations (e.g. banks branches, microfinance institutions) [6]. A similar analysis of agents in Tanzania conducted by Financial Sector Deepening Tanzania (FSDT) found that 80% of mobile money agents were within five kilometers of a bank, MFI or ATM [7]. These analyses were largely supported by surveys of mobile money and bank agents in East Africa by the Helix Institute from 2013-2015, which showed that only 22%-30% of agents were rural despite the majority of the population in surveyed countries living in rural areas.

In 2016, UNCDF began working with agricultural value chains in Uganda and demonstrated that there were viable business models for having agents in extremely rural environments, (some even more than seventy kilometers away from any urban environment) as long as there was enough economic activity in the location. These can be considered “rural oases”, which are outside urban areas, yet have significant amounts of economic activity driven by things like markets, a fuel station on a highway, or high densities of cash crops. In the Pacific this would likely also include villages where mineral rights or other land use payments are being made to rural communities or where agents were supported by diary or coffee businesses. Analyses done by The Boston Consulting Group (BCG) in 2017 found that 85% of viable agents in rural areas were located in a “rural oasis” like these [8].

Therefore, in the South Pacific we should understand that most system usage will be in urban environments, and extending these models into rural areas beyond the economic oases supported by coffee, mineral rights or other land use payments will be difficult and largely unprecedented.

Conducting a TAM analysis that focuses on high potential customers -- defined as urban adults -- shows that the small population sizes in PICs combined with the high proportions of their populations living in rural areas exacerbates the business case. While there is a precedent for countries with smaller urban adult TAMs than PNG and Fiji, for the rest of the PICs in the analysis, TAMs range between 90,000-20,000 urban adults, which is 8.5 times smaller in Tonga and Samoa than the TAM of any other successful country.

Total Addressable Market for Urban Adults

The Future of Financial Inclusion in the Pacific

The general conclusion of this analysis is that scaling financial services to the mass markets of PICs is difficult and unprecedented. It pushes the business case behind mobile money and agent banking farther than has ever been shown to be successful in the past for the countries of Solomon Islands, Vanuatu, Tonga and Samoa. This does not mean the models cannot function in these environments, it means that for them to work, a concerted effort is needed to enable them. Three of the most important of which include:

1. Given the small populations, there needs to be focus on increasing transactions per customer on these systems. Governments can support these systems by encouraging their usage for utility payments, government salary payments, relief and social welfare payments, tax payments and transportation payments.

2. Having competing providers in many of these markets will exacerbate a difficult business case by further dividing an already small addressable market. Therefore, efforts should focus on complementary partnerships, especially between banks and telecoms. Further, PICs may want to develop regionally aligned policies that facilitate companies serving customer bases across countries and sharing infrastructure like agent networks within them.

3. Public sector funds should be used to help companies understand where rural oases are located, and how their business models need to be augmented to determine how far they might be extended beyond these locations to where the majority of Pacific Islanders live.

Sources:

[1] https://www.cgap.org/blog/good-things-come-small-packages-mobile-money-fiji

[2] Expert interviews with former and current employees of these services.

[3] Somaliland is not included in this analysis. Eswatini is added to this analysis even though it is

[4] https://www.mckinsey.com/industries/financial-services/our-insights/mobile-money-in-emerging-markets-the-business-case-for-financial-inclusion

[5] This assumption is extremely optimistic given only four countries in the world have adult penetration rates over 50%.

[6] https://cenfri.org/publications/the-evolution-of-agent-networks-in-africa/

Mas, Ignacio and Elliott, Andrew, Where's the Cash? The Geography of Cash

[7] Points in Tanzania (November 11, 2014). FSDT Focus Note, No. 2, 2013. Available at SSRN: https://ssrn.com/abstract=1875883

[8] https://www.bcg.com/publications/2019/how-mobile-money-agents-can-expand-financial-inclusionnot covered by Findex 2017.