UNCDF supports

DIGITAL

Finance and Solutions

that build resilient lives and economies

Access to Digital Financial Services is an enabler to

12 of the SDGs

Digital Finance is a Gateway to

Financial Inclusion

Since 2009, UNCDF has been supporting digital finance in developing economies across Africa, Asia and the Pacific.

By providing a mix of policy, technical and financial support, we have contributed to reaching nearly 8 million people who are now actively using digital accounts from Samoa to Sierra Leone.

Today customers from these markets are using digital accounts from banks, mobile money and payment service providers for payments, savings, credit and insurance. Many use these services to access energy, pay school fees and receive social transfers.

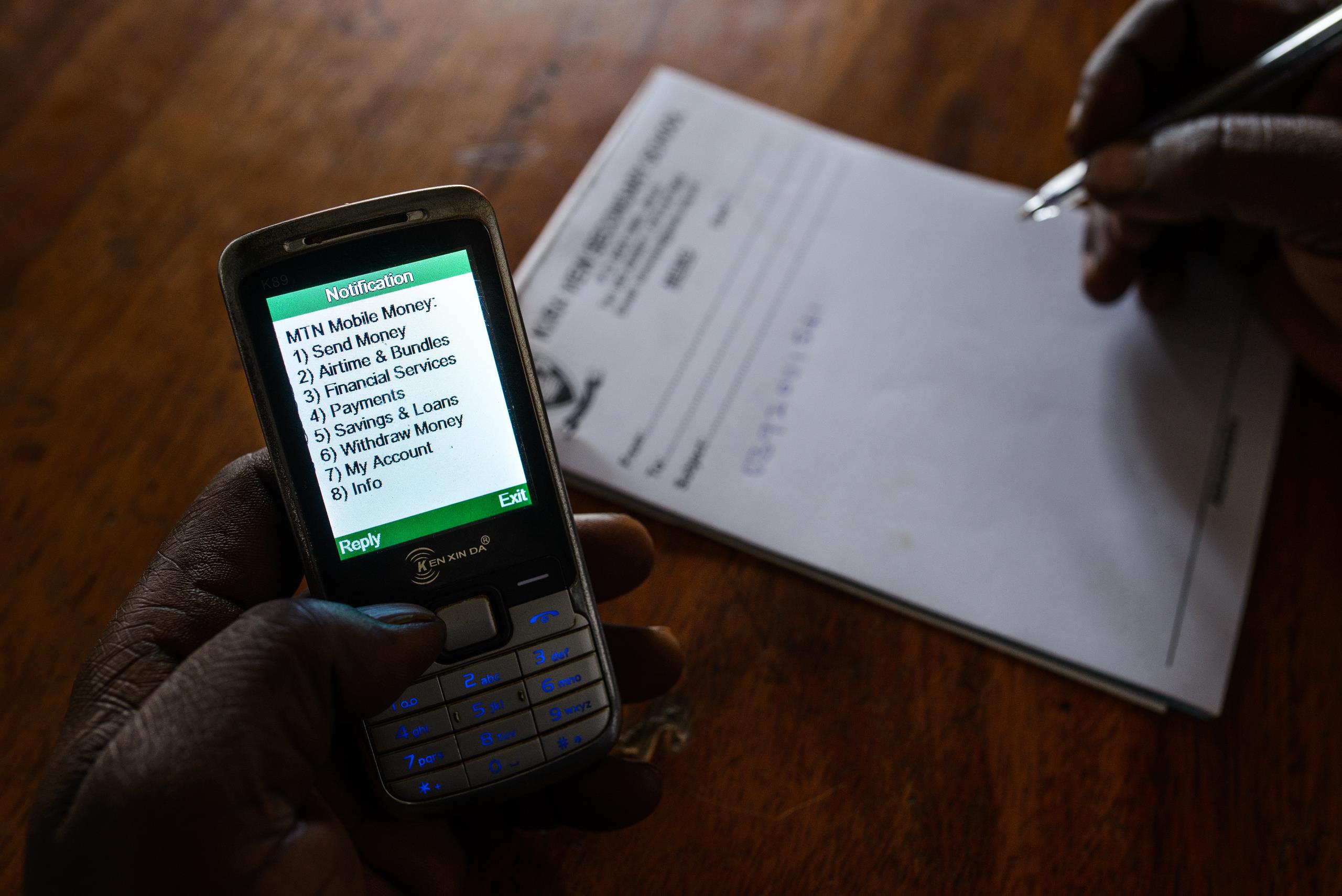

Digital financial refers to a range of formal financial services accessible via digital accounts through a distribution network.

Customers usually access their access their account using a mobile phone or card in combination with an agent, merchant or ATM. Digital finance requires an ecosystem of cooperating private and public actors to function properly.

Digital solutions are digital applications that solve problems or create opportunities. When linked with digital finance, they can help overcome some of the challenges of digital finance by providing better management tools, financial education, and pay-as-you-go solutions for water and energy.

They can also help solve specific sustainable development goals, such as better health information, quality education and more sustainable cities and communities.

New DFS Users

Least Developed Countries

New Policies

Implemented

Projects

Implemented

Professionals in the Community of Practice

|

|

|

|

|

|

High Volume |

Customers |

Distribution |

Providers |

Policy and Regulations |

Infrastructure |

GET THE LATEST UPDATES TO YOUR INBOX